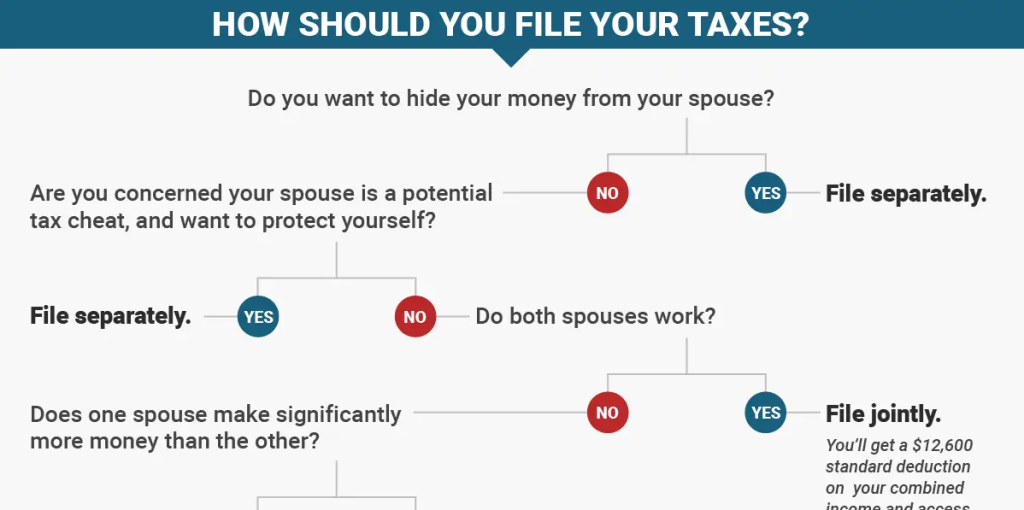

What is it?

Married filing separately is an option available to all married individuals when choosing a filing status for their federal income tax returns. Your filing status is important because it determines, in part, the amount of your standard deduction, the deductions and credits that are available to you, and the amount of your correct tax for the year. When filing a joint return, you and your spouse combine all income, exemptions (personal exemptions are suspended for 2018 to 2025), deductions, and credits. When filing separate returns, you report and pay tax only on your own income and take credit only for your own deductions and credits.

Who can file a married filing separately return?

You must be considered married for the tax year

In order to file a married and separate return for a given tax year, you must be considered married for that tax year. You are considered married for the tax year if you are married on the last day of the year.

You have not already filed a joint tax return for the year

Once you file a joint return, you cannot file an amended tax return to change your filing status to married filing separately after the due date of the tax return (usually April 15). If the due date has passed, it’s too late to change your mind.

Reporting income, deductions, exemptions, and credits on separate returns

General rule

When you file married and separate, you must include all income that you individually earn or receive. This includes wages and self-employment income. If you are deemed to own property under the laws of your state, you report any income that the property generates on your separate return. If you own property jointly with your spouse, you report a portion of the income generated by the property (based on your share of ownership). So, if you own the property equally, you will each report one-half the income generated by the property.

Similarly, you report only exemptions (personal exemptions are suspended for 2018 to 2025), deductions, and credits to which you are individually entitled. You may be able to claim deductions on your separate return for expenses that you paid jointly, but special rules apply, and you should refer to IRS Publications 501 and 504.

Special rules for community property states

If you live in a community property state (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), you will need to familiarize yourself with local law. (You may also be able to elect community property treatment under Alaska law.) The general rule in community property states is that you and your spouse split community income equally when you file separate returns. Community income includes wages earned by either you or your spouse during the marriage, as well as income from any community property. (Generally, this is property that you or your spouse acquired during marriage while living in a community property state.)

You and your spouse live in a community property state that considers wages earned during a marriage to be community income and requires such income to be split evenly. Your spouse earns $100,000 a year in wages, while you are not employed. If you and your spouse file your federal tax return as married filing separately, each of you will report $50,000 in wages.

If you and your spouse have not lived together at all during the tax year, special rules apply, and you should consult a tax professional.

Any deductions paid from community funds must be divided evenly if you and your spouse file separately.

Advantages

You don’t need your spouse’s consent

Unlike filing jointly, you don’t need your spouse’s consent to file a separate federal income tax return. Further, you don’t have to wait for your spouse to file his or her own return.

Separate liability

If you file separately, you are responsible only for the taxes on your own return.

If you are contemplating separation or divorce, the importance of this factor should not be underestimated. Imagine receiving a notice from the IRS two years after your divorce is final, explaining that you owe money because your spouse didn’t report some earnings on a joint tax return that you filed.

In certain situations, filing separate returns can result in less total tax

Generally, filing separately results in a higher combined tax liability for you and your spouse than if you file jointly (see discussion in the section on disadvantages, below). However, in some circumstances, filing separate returns can actually result in a lower combined tax liability.

This occurs because some deductions are allowed only when they rise above a certain amount (determined as a percentage of adjusted gross income). Medical expenses, casualty losses, and miscellaneous itemized deductions (miscellaneous itemized deductions subject to a 2 percent floor are suspended for 2018 to 2025) are deductible only to the extent that they exceed a specific percentage of income. Filing separate returns reduces the income on each spouse’s return. Because the income on each return is less than it would be on a joint return, the amount that these deductions have to exceed to be deductible is reduced as well.

Ken and Sue are married, and each earns $100,000 in 2024. They pay $10,000 in state tax during the year, have deductible home mortgage interest of $11,000, and make $4,000 in charitable contributions. Sue has $20,000 in medical expenses.

(1) If Ken and Sue file jointly:

| Their combined adjusted gross income is $200,000 | $200,000 |

|---|---|

| Medical expenses are deductible only to the extent that they exceed 7.5% of adjusted gross income (7.5% of $200,000 = $15,000), so the amount of medical expenses that can be deducted is $5,000 ($20,000 – $15,000). | $5,000 |

| All other itemized deductions total $25,000. | $25,000 |

| When these itemized deductions are subtracted from adjusted gross income, Ken and Sue are left with $170,000 in taxable income for tax year 2024. | $170,000 |

| Tax | $27,506 |

(2) If Ken and Sue file separately:

Ken:

| Adjusted gross income is $100,000 | $100,000 |

|---|---|

| Itemized deductions (half of state taxes paid, half of home mortgage interest, half of charitable contribution) total $12,500. | $12,500 |

| Taxable income of $87,500 | $87,500 |

| Tax | $14,303 |

Sue:

| Adjusted gross income is $100,000 | $100,000 |

|---|---|

| Itemized deductions – Medical expenses ($20,000) are deductible to the extent that they exceed 7.5% of adjusted gross income (7.5% of $100,000 adjusted gross income is $70,500), so deductible medical expenses are $12,500 ($20,000 less $70,500). When Sue adds half of state taxes, half of the home mortgage interest, and half of the charitable contribution, her itemized deductions total $25,000. | $25,000 |

| Taxable income of $75,000 | $75,000 |

| Tax | $11,553 |

Filing separately, the couple’s total tax ($25,856) is less than if they had filed jointly ($27,506).

The only way to know for sure which filing status will give you the lowest total tax is to do the calculations both ways (jointly and separately) and compare the results.

If you know that you’re going to file separate returns, consider doing a little planning. You can decide ahead of time who is going to pay what deductible expenses.

You can change your mind

If you or your spouse (or both) file separate returns, you can change to a joint return any time within three years from the due date (not including extensions) of the separate returns.

To change your filing status to married filing jointly, you and your spouse must complete and file Form 1040X, Amended U.S. Individual Income Tax Return.

Disadvantages

Filing separately is more complicated

Unlike filing a joint return, in which you simply combine all income and deductions, filing separate returns entails allocating income and deductions between you and your spouse. If you live in a community property state, you’ll have to split income and deductions.

Generally, filing separate tax returns results in more total tax than filing jointly

Most married couples pay more total tax when they file separately than when they file jointly. This is because the tax rate is effectively higher if you file separately. In addition, any of the factors discussed below could result in greater total tax.

The only way to know for sure which filing status will give you the lowest total tax is to do the calculations both ways (jointly and separately) and compare the results.

Availability of tax credits and deductions is reduced

If you file separately, you cannot take the earned income credit (a refundable credit available to individuals who qualify based on income and family situation). Your ability to take advantage of the credit for child and dependent care expenses and the credit for the elderly and disabled is also significantly limited. Further, you can only take deductions for expenses that you actually paid, and filing separate returns affects your ability to claim dependent exemptions in some situations (personal and dependency exemptions are suspended for 2018 to 2025),.

If your spouse itemizes deductions, you have to itemize as well

If you file separately and your spouse itemizes deductions, you must also itemize, even if your total itemized deductions are less than the standard deduction you would otherwise be entitled to.

You file a separate tax return, and your spouse itemizes deductions. The standard deduction for an individual who files separately is $14,600 in 2024. You have total itemized deductions of $1,000. Since your itemized deductions do not total more than $14,600, you would normally take the standard deduction. However, your spouse itemizes deductions, so you don’t have a choice. You have to itemize, taking a deduction of $1,000.

Larger portion of Social Security benefits may be included in income

If you file separately and lived with your spouse during any part of the year, a larger maximum percentage of your Social Security benefits (85 percent) may have to be included in your income.

Negative impact on ability to take advantage of IRAs

If you file separate returns, your ability to make deductible contributions to a traditional IRA is reduced. Furthermore, your ability to contribute to a Roth IRA is limited.

You can’t make spousal IRA contributions

Spousal IRA contributions are contributions made to an IRA for a nonworking spouse or a spouse with little income. You can’t make such contributions if you are filing separate returns.

Reduced ability to exclude income

When you file separately, the benefit of the $25,000 passive loss allowance for actively managed rental real estate may be reduced or eliminated. Additionally, no exclusion is allowed for interest on EE savings bonds (may also be called Patriot bonds) used for higher education expenses.

Married couples may pay more total tax than they would if unmarried filing as single individuals (“marriage penalty”)

The total tax of two unmarried individuals (each filing as single) may be less than the total tax if the two individuals are married, whether they file jointly or separately. This is particularly true when the two individuals have relatively equal incomes. This is often referred to as the “marriage penalty.”

The marriage penalty can occur, for example, when the tax code provides tax brackets that are wider but not twice as wide as those for single filers.

Not all married couples experience a marriage penalty. In fact, where one spouse earns significantly more than another spouse, filing a joint return will often result in tax savings.

]]>